Our Call to Action

Delivering a vision of affordable flood insurance

This section explains Flood Re’s approach to transition. It sets out Flood Re’s operating model and explains how its success to date has been achieved through partnership with the insurance industry and Government. It explains the importance of a fixed end date and how climate change may mean the model becomes harder to sustain as we approach this date. Finally, it sets out Flood Re’s Theory of Change, and how Flood Re uses its position to act as a wider catalyst of change in order to achieve its transition vision.

Flood Re’s Theory of Change

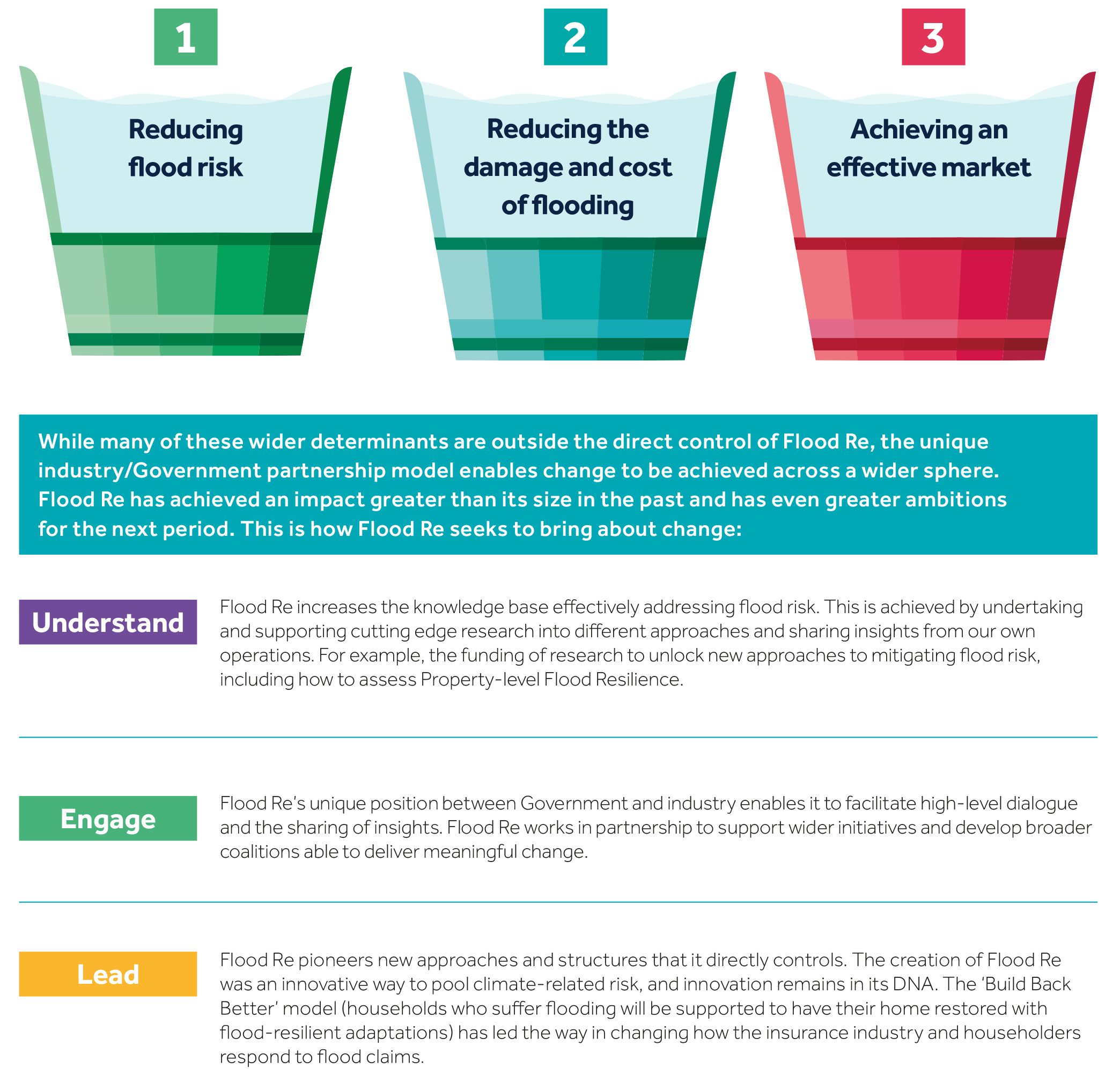

Flood Re’s vision is for a market where householders at risk of flooding can obtain affordable home insurance without the existence of Flood Re from 2039. Realising this vision is dependent on a wide range of factors, mostly outside of Flood Re’s direct control. Since 2020, to track progress across the issues impacting on flood insurance availability, Flood Re has created a set of indicators for each of the three transition ‘buckets’ outlined below. Flood Re’s Annual Report includes a dashboard to assess progress for each bucket, as part of our wider commitment to be transparent about the inherent challenges involved in Flood Re’s exit from the market.

This section explains progress against each of these indicators in greater detail, as well as the work Flood Re has undertaken to support progress in each area.

Flood Re’s three transition buckets

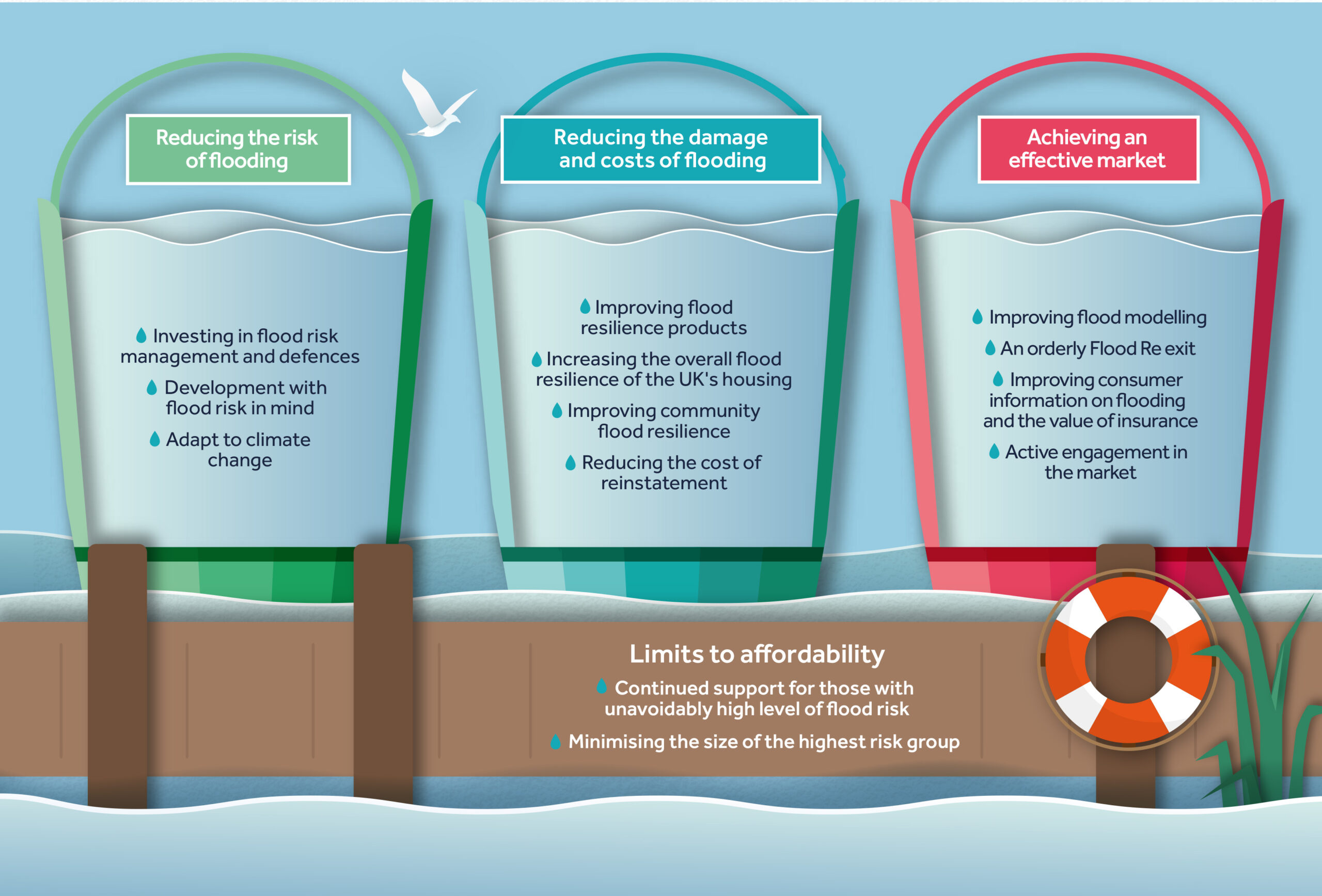

As outlined in the previous section, achieving a flood insurance market which is both risk-reflective and widely affordable is a significant challenge requiring action on a number of fronts. This section outlines the action needed to achieve Flood Re’s vision.

The core challenge is to reduce the overall risk of flooding despite climate change. This will require a step-change in approach. Currently most flood defence spending is focused on reducing long-standing flood risk in the UK. But climate change will increase the overall level of flood risk and give rise to increased unpredictability in weather patterns. So current action is not enough.

The two priorities remain investment in large-scale flood defences and a focus on drainage systems (which require both investment and maintenance). However, there is growing recognition that not every area can be protected and with climate change increasing the unpredictability of weather patterns, the UK will need greater overall flood resilience and adaptability. This means PFR and NFM will both have important roles to play. Flood Re wants to see innovation in managing floods and a system wide approach encompassing government at all levels, the private sector and individual households. All these parties have a role to play in reducing flood risk, and all benefit from reduced flood risk. There are also wider benefits to the UK economy of being at the forefront of climate change adaptation. This section outlines the challenge, how we meet it, and the benefits of doing so.

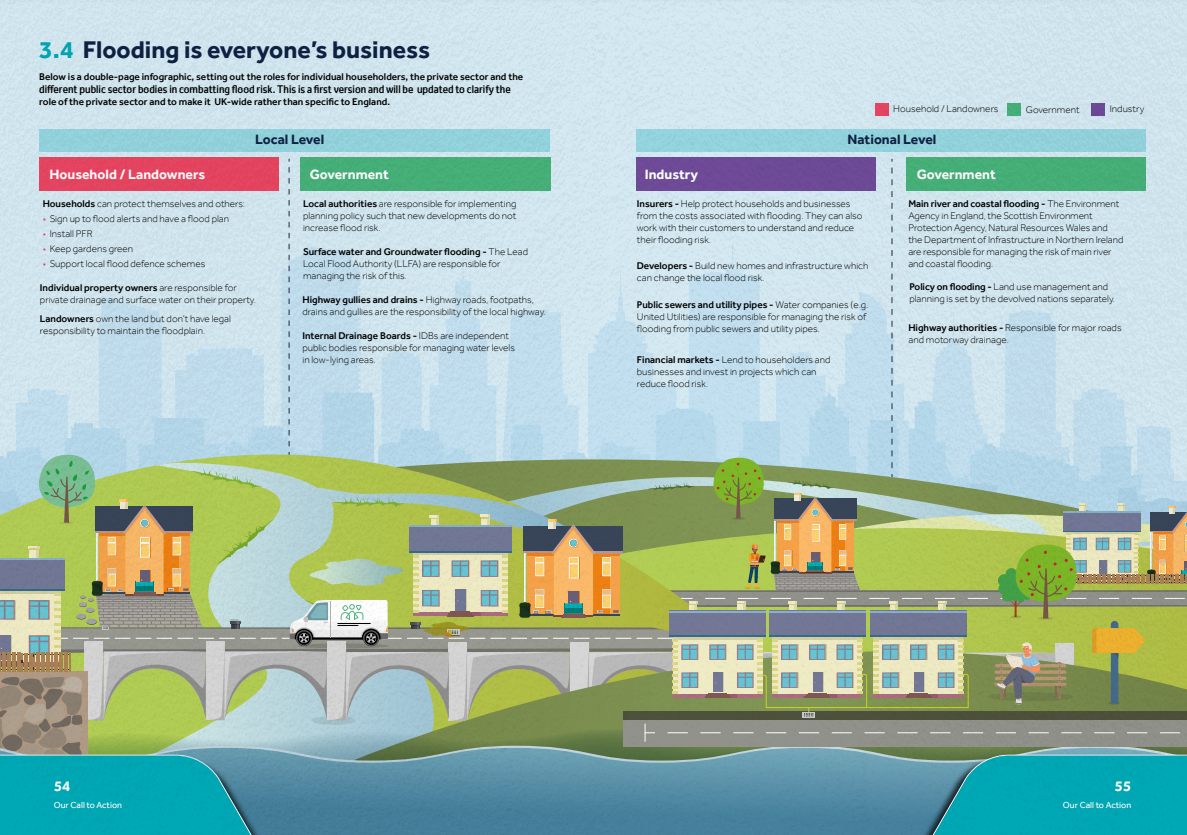

Flooding is everyone’s business

Everyone benefits from managing flood risk

As set out in Section 1, Flood Re will cease to exist in 2039, and household flood insurance will transition to risk-reflective pricing. How many households face increased premiums, and by how much they increase, will depend on the overall level of flood risk facing UK domestic properties in 2039.

Flood Re is a small organisation but has shown through initiatives introduced under the auspices of the previous Transition Plan, it has the potential to catalyse bigger changes across Government and industry. This section outlines Flood Re’s plans for the next period. The ambitions are high. The challenge is considerable and urgent, but it is also being recognised by a growing number of partners. Flood Re is committed to using its expertise, experience and resources to act as a catalyst for change at the national, local and household level.

This section explains what Flood Re will do, and why.

Section 4 outlines the commitments Flood Re is making to support its vision for transition

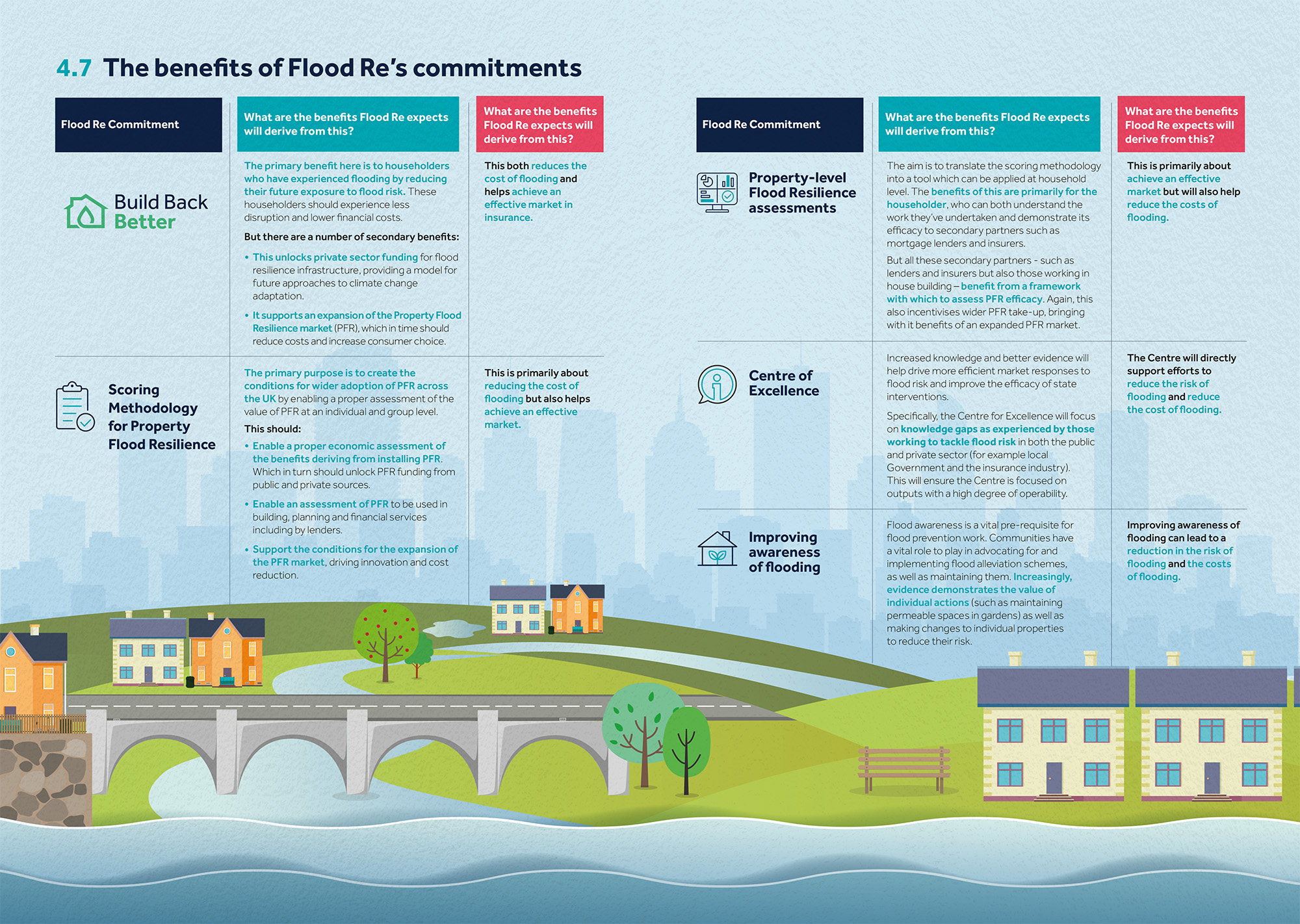

The benefits of Flood Re’s commitments

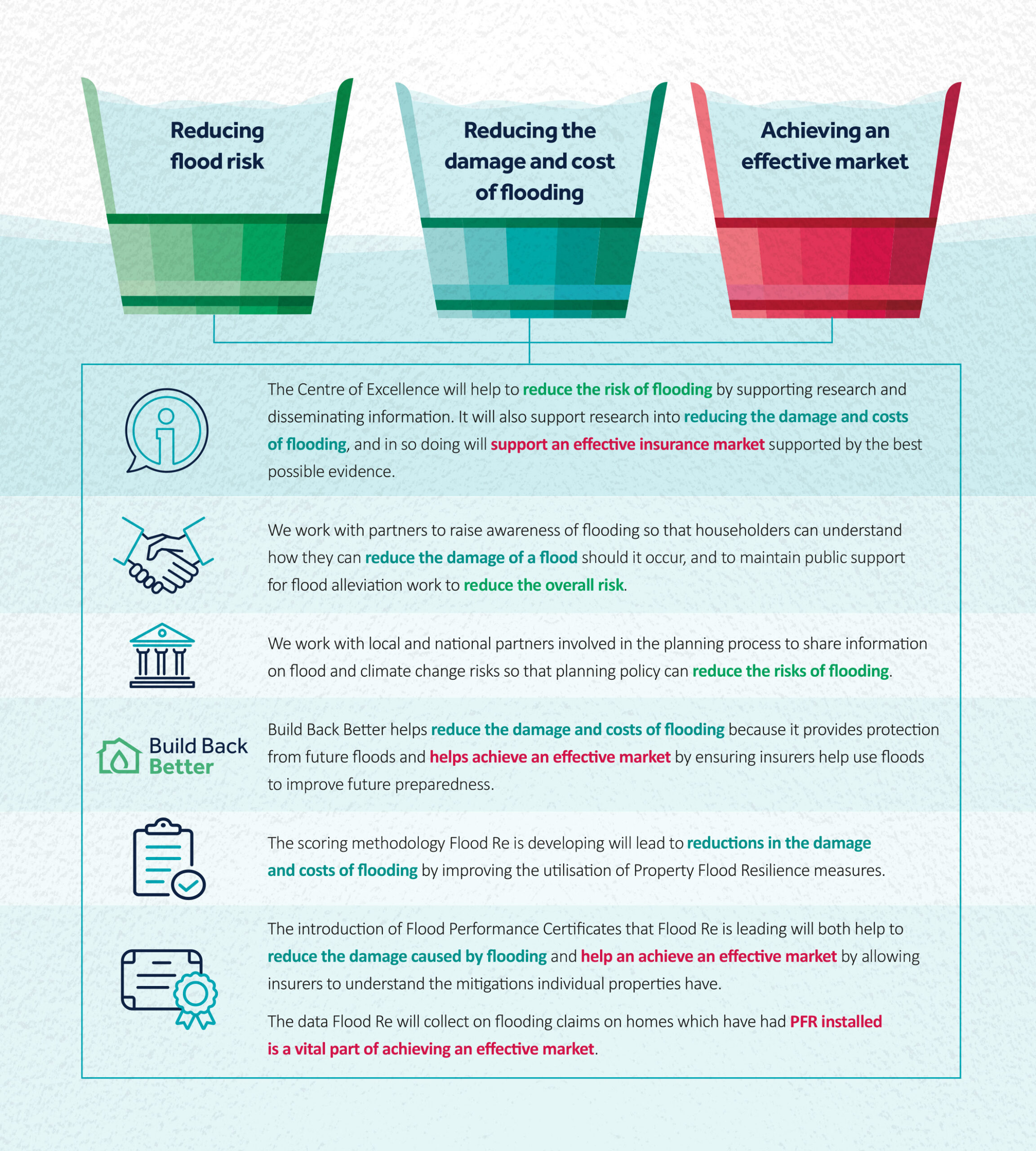

Flood Re’s commitments support the Three Buckets

Read the full Transition Plan to learn more about the actions that Flood Re and others will need to take, to make the transition to an affordable and risk-reflective market for household insurance, more achievable.